HolonIQ's Year in Edtech: Year of the Unicorn

With 61 $100M+ Funding Rounds in 2021, there are now Edtech Unicorns Everywhere

Australian firm HolonIQ has emerged in the last few years as one of the most insightful and useful market intelligence platforms for the Edtech sector.

While true access to the HolonIQ database and platform starts at $20,000 and is designed explicitly for venture capitalists, the public reports, charts, articles and events it puts out provide a surprisingly thorough globalized overview of the space.

Yesterday, HolonIQ put out its annual report for the “Global Edtech Venture Capital Report” for 2021, and the result is that 2021 was yet another banner year for Edtech, due in no small part to the COVID pandemic’s disruption of global education systems.

In this short article, we’ll go through a few of the top takeaways of the report (which is certainly worth reading in its entirety), as well as begin to meet the rapidly growing list of Edtech unicorns” (unicorns being Silicon Valley-ese for companies with market valuations over $1B.)

Takeaway 1: Edtech Investment is Breaking Records in the US, EU and India

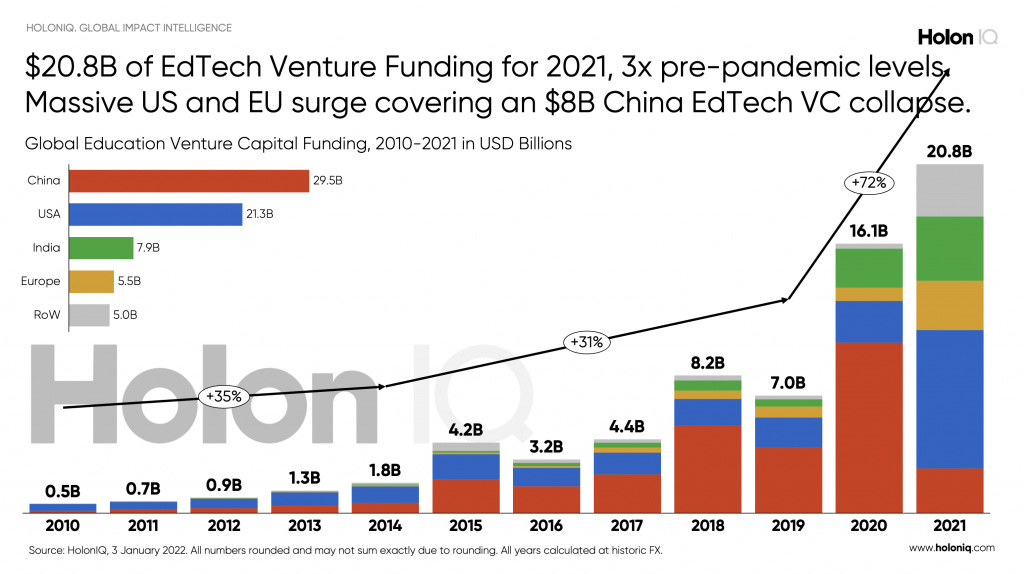

Edtech investment is breaking records all over the world, with over $20 billion dollars in total investment going into the sector in 2021. To put this in perspective:

“Once a niche sector with an ambitious vision to transform the way the world learns, EdTech Venture investment is now 40x larger than it was a little over a decade ago in 2010, nearly 5x the previous investment peak in 2015 and 3x pre-pandemic investment levels in 2019.” - HolonIQ

While past HolonIQ reports often focused on the huge levels of investment in the Chinese edtech market over the last decade, the regulatory crackdown in China this year and the uncertainty about the future of the sector put a massive chill on the prospects of foreign VC-backed Edtech companies in China.

On the other hand, the Indian market continues to explode in investment in the post-pandemic era, and this year saw massive growth in the European market (spearheaded by specialist investors such as Brighteye Ventures and Emerge Education). US investment in edtech was also enormous this year,

The rest of the world is starting to catch Edtech fever as well; investment in Edtech has accelerated, with almost all of the $5 billion dollars overall invested in the last decade being invested in 2021, including investments in fast-growing companies like Indonesian Ruangguru, Australian startups Forage, Vivi and Adventus, Israeli Joytunes, and Brazilian Hotmart, among (many) others.

Takeaway 2: Chinese Edtech has been upended by regulation

Note the sliding scale of the charts above; until 2021, Chinese Edtech utterly dominated the world. In 2020, it received $10B+ of the $16B dollars of investment.

The description of the Chinese regulations provided in this report is one of the clearest overviews I’ve seen, so I will quote it at length here, and add some highlights of some of the most chilling provisions. In essence, the Chinese government — perhaps threatened by the massive 2020 investment in edtech companies looking to break into the massive Chinese market for tutoring, k-12 schooling and English language learning— has moved to both socialize and nationalize the edtech sector:

China’s clear EdTech investment leadership position rapidly unravelled through 2021 as the Chinese government initiated a broad range of policies that undermined the fundamental model accelerating EdTech in the country. Chinese companies teaching academic curriculum must go non-profit, cannot pursue IPOs, or take foreign capital. All vacation and holiday curriculum tutoring is off-limits, online tutoring and school-curriculum teaching for kids below six years of age is forbidden and agencies must not teach foreign curriculum or hire foreigners outside of China to teach. Listed companies are prohibited from issuing stock or raising money in capital markets to invest in school-subject tutoring institutions, and foreign firms are banned from acquiring or holding shares in school curriculum tutoring institutions. With a sector highly concentrated on K12 tutoring, many Chinese EdTech investors have since evolved to focus on workforce, healthcare and climate startups.

Takeaway 3: Edtech Funding Rounds Are Getting Bigger

Moreover, the funding rounds seem to be getting bigger, with a record number of ‘mega-rounds’ (investment rounds of $100 million dollars or more) occurring in the sector.

HolonIQ calls out a number of megarounds in particular of note:

🇺🇸 Articulate‘s $1.5B Series A, 🇮🇳 Eruditus‘ $650M Series D, 🇮🇳 Unacademy‘s $440M Series H, 🇨🇳 Fenbi‘s $390M Series A, 🇺🇸 Course Hero‘s $380M Series C, several $300M rounds in 🇺🇸 BetterUp‘s Series C, 🇺🇸 Age of Learning‘s Series C and 🇨🇦 ApplyBoard’s Series D, 🇦🇹 GoStudent‘s $244M Series C and 🇺🇸 Masterclass‘ $225M Series F.

The report also states that there were more than 3,000 funding rounds over $5 million dollars, mostly to seed or early stage companies. This bodes well for the future of edtech. With so many irons in the fire for VCs, and so many young entrepreneurs moving into the space, a significant number of early-stage companies will either grow into larger players themselves or be scooped up in acquisitions.

Takeaway 4: Unicorns are Multiplying Like Rabbits

Silicon Valley in general, and HolonIQ in particular, love to focus on how many ‘unicorns’ are created each year. The phrase ‘unicorn’ was once a reference to the extreme rarity of VC-backed privately held startups that are valued at a billion dollars or more.

According to Edtech reporter Henry Kronk’s great report on Edtech unicorns: “When Cowboy Ventures founder Aileen Lee coined the term in 2013, the world had only 39 startups valued at $1 billion or more. Today, CB Insights counts 465.”

In Edtech, the number of unicorns has exploded in the last three years, almost doubling in 2021 alone, along with several IPOs for 2019 unicorns (technically, an IPO removes a company from the unicorn list, because it the company is not then privately-held):

Notice that seven of the 11 unicorns pre-2018 were in the Chinese market- precisely the market that has been capsized in 2021. A prime example is VIPKid (Unicorn class 2016), a company that grew enormously by offering English language tutoring for Chinese students by foreign teachers, exactly the type of foreign-teacher tutoring that is now banned; VIPKid had to end its flagship program in October of 2021.

On the other hand, US and Indian unicorns are suddenly everywhere (along with Byju’s, the only Edtech ’decacorn’).

Of the 22 Edtech Unicorns spawned in the pandemic era (2020-2021):

14 are US-based

1 is Australian (corporate learning platform Go1)

1 is Israeli (music-learning app creator JoyTunes)

1 is European (Austrian tutoring platform GoStudent)

1 Chinese (YunXueTang, an enterprise training platform exempt from the government regulations)

FWIW, I would predict that the 2022 unicorn list may contain several more European startups, like fast-growth Poland-based Brainly or UK-based Multiverse, as well as its first Latin American edtech company. Edtech Insiders will do some deeper dives on the Edtech unicorns (too many of which are still unknown to US audiences- present company included.)

The HolonIQ report is a timely reminder of the banner year that was in Edtech, and the of the huge bets that the world is placing that the future of learning will continue to be online.